Advantages of using Actual Cost with Lot/Serial Items.

Products using Lot or Serial control are unique as they are capable of distinguishing a difference between one individual instance (Serial) or group (Lot) of the same product, in the same warehouse, from another. This allows for an exclusive Cost Method called Actual Cost (see Inventory Cost Methods) to be used. As Lot/Serial numbers must be entered on any transaction where a Lot/Serial controlled product is used, it is possible to capture a more accurate Cost of Goods Sold than the Average, Standard or layer-based Cost methods are capable of. Actual Cost is just what it sounds like, the actual cost associated with that specific Serial or Lot number of a given product, in a given warehouse. Actual Cost allows for a single product to have multiple costs associated with different Lot/Serial Numbers, providing the most accurate Cost Of Goods Sold possible. This article will go over the advantages of using Actual Cost and disadvantages of other Cost Methods for Lot/Serial controlled products.

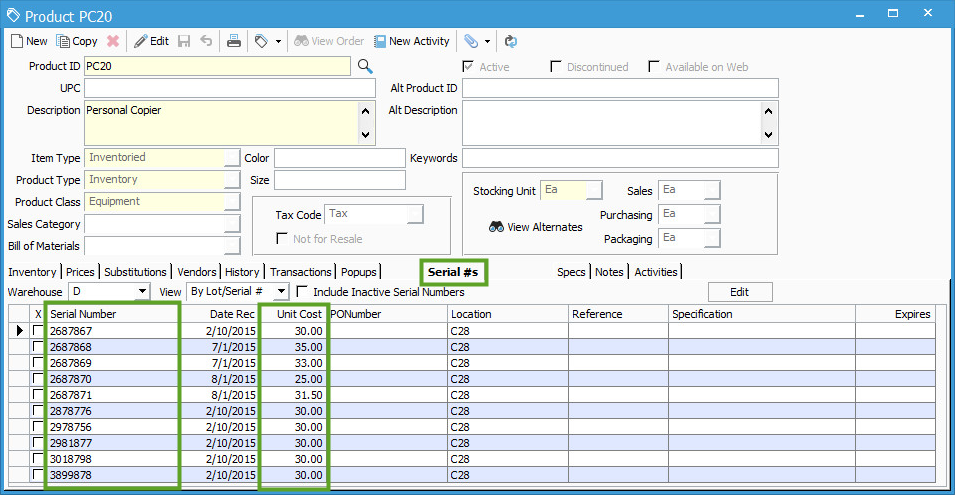

Notice the example in the screenshot below. PC20 is a serial controlled product, you can see on the Serial #’s tab that a unique Unit Cost is associated with each individual Serial Number.

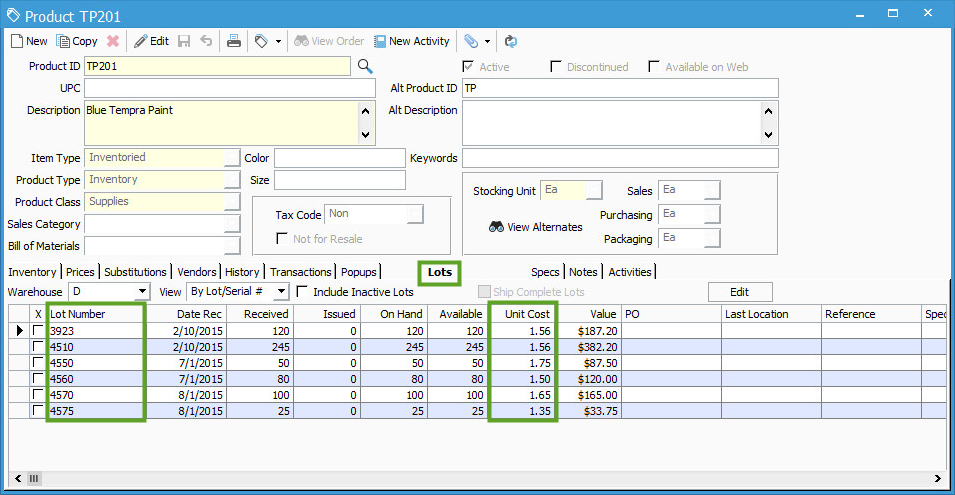

Notice in this second screenshot, product TP201, which is a Lot controlled product. This time on the Lots tab, you can again see that a unique Unit Cost is assigned to each Lot Number for this product.

The Unit Cost, shown above, is defined by whatever cost was entered on the Inventory Receipt that brought the associated Lot/Serial number into inventory.

The major advantage of capturing Actual Cost associated with a Lot or Serial number comes when the product is sold (See the Sell Lot/Serial Numbered Products article).

Using the products above, for example, selling product PC20 will require that I enter a serial number on the Sales Order. Using Actual Cost, if serial number 2687867 (first line) is entered, the Cost Of Goods Sold will be $30.00 each, as that is the cost associated with that specific serial number. If serial number 2687868 (second line) is entered, the Cost Of Goods Sold will be $35.00 each.

The same is true for the Lot controlled product. If TP201 is added to a Sales Order, a Lot number must be entered. Using Actual Cost, if Lot 3923 is entered (first line) the Cost Of Goods Sold will be $1.56 each. If Lot 4550 is added (third line), the Cost will be $1.75 each.

The advantage of using Actual Cost vs a Layer Based Costing method (FIFO/LIFO) is that Cost Layers have no relationship to a Lot or Serial number the way Actual Cost would. When adding a Lot/Serial controlled product to a transaction, such as a Sales Order, a Lot/Serial number is required for that product, which is selected by the user. The user is free to enter any Lot/Serial number that is available in a given Warehouse/Location, regardless of Cost Layer. However, when adding that Lot/Serial number, the system will still use whatever cost layer is oldest with available quantity, whether that that was the layer that Lot/Serial was received in on or not.

The advantage of using Actual Cost vs Average cost is that Average cost will just use an average of previously posted transactions instead of a specific cost related to the Lot or Serial number (see the Average Cost Method article).

The advantage of using Actual Cost vs Standard Cost is that Standard cost will use the same, user defined cost every time, regardless of the cost that you actually received that Lot/Serial number at.

Setting Actual Cost as the cost method for your Lot/Serial controlled products will ensure that the most accurate Cost Of Goods Sold possible is captured for that product on every sale, every time.